Driving With No Insurance? Fines, Tickets & Penalties You Need to Know in 2026

Driving without insurance in the United States has long been illegal. However, in 2026, enforcement became stricter and more automated.

States now use electronic verification to quickly catch uninsured drivers, and penalties have become harsher. What was once often a simple fix-it ticket can now mean serious fines, license suspensions, and other consequences.

We will cover what happens if you are caught driving uninsured, how fines work across states, and what you can do if you receive a ticket.

Key Facts:

- Auto insurance is required in nearly all U.S. states, with minimum liability coverage typically including bodily injury and property damage.

- First-offense uninsured driving fines in 2026 generally range from $100 to over $1,500 depending on the state.

- Repeat uninsured driving offenses can result in fines exceeding $2,000 plus license suspension and vehicle impoundment.

- Many states use electronic insurance verification systems to detect uninsured vehicles in real time.

- SR-22 filings are commonly required after violations, typically lasting 1 to 3 years as proof of financial responsibility.

- License and registration suspension can occur immediately after a confirmed uninsured driving violation in most states.

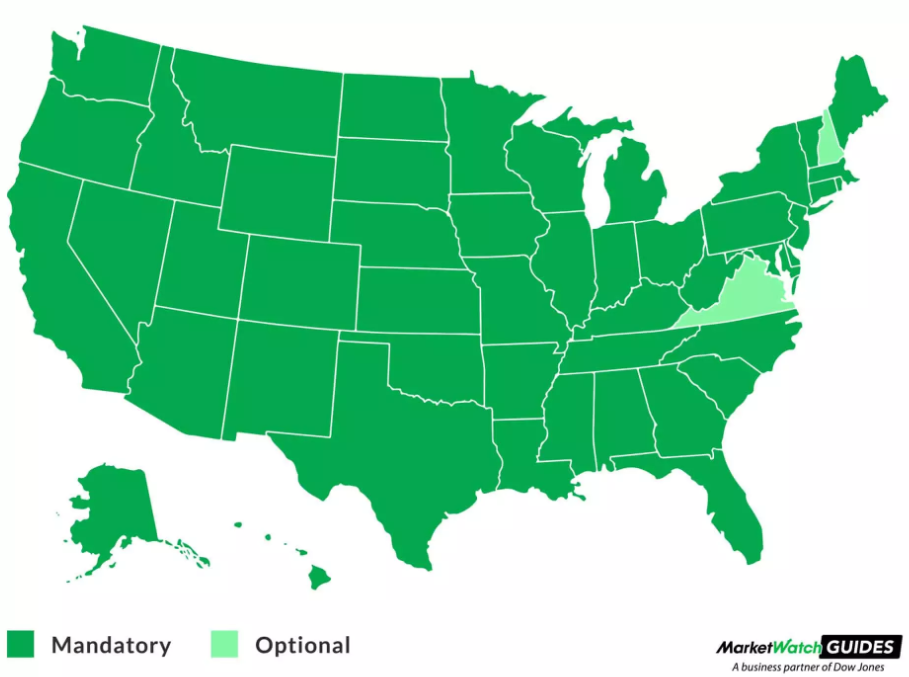

Is Insurance Legally Required in All States?

Almost all U.S. states require drivers to carry active auto insurance before operating a vehicle on public roads. Minimum coverage levels vary, but they typically include bodily injury liability and property damage liability.

A small number of states allow alternatives such as financial responsibility bonds, but these are tightly regulated and not common for everyday drivers.

Examples include:

- New Hampshire: Does not require mandatory auto insurance for private passenger vehicles but requires proof of financial responsibility, which can be met with a bond or cash deposit instead of insurance.

- Virginia: Allows certain drivers to post a cash deposit or bond with the DMV as an alternative to carrying insurance in limited cases.

You May Also Like: What Happens After a DUI? Laws, Penalties, and Violations

For commercial drivers, personal assumptions do not apply. If you are operating a vehicle that is not properly insured under a valid policy, enforcement agencies treat it as uninsured driving even if you believed coverage existed through an employer or lease arrangement.

Caught Driving Without Insurance: What Happens Next?

A ticket for driving uninsured usually begins at a traffic stop or roadside inspection. Thanks to electronic insurance verification systems now in place in most states, law enforcement officers can instantly check if your coverage is active.

If you’re flagged as uninsured, here’s what you might face:

- an immediate fine,

- a requirement to show proof of insurance in court,

- administrative action by the DMV.

If valid insurance did not exist at the time of the stop, showing proof later rarely cancels the violation. Courts generally rule based on coverage status at the moment of enforcement.

Since penalties vary widely depending on the state you’re driving in, it’s worth looking at how those differences play out in real situations.

How Much Can You Be Fined for Driving Without Insurance?

Penalties Beyond the Ticket: What Else You Face

The fine is often the smallest part of the problem. Most states impose additional penalties that directly affect your ability to drive legally.

License suspension is common after a no-insurance ticket, especially for repeat violations. Suspension periods range from 30 days to multiple years. In some states, reinstatement requires proof of continuous insurance for a fixed period.

Registration suspension is also widely used. Plates may be confiscated or flagged, making the vehicle illegal to operate even if insurance is later purchased.

SR-22 filings are another major consequence. This is not insurance itself, but a state-mandated proof of coverage that insurers file on your behalf. SR-22 policies are expensive and typically required for one to three years.

What Happens If You Get Into a Crash Without Insurance?

Accidents without insurance coverage are financially and legally catastrophic. Here’s what happens:

1. Full personal liability: You become responsible for all damages, including vehicle repairs, medical bills, and third-party property damage, which can easily total tens of thousands of dollars.

2. Medical and legal claims: Injured parties can file lawsuits against you, potentially leading to judgments, wage garnishments, or liens on your property that can last for years.

3. Automatic license suspension: Many states impose license suspensions ranging from six months to over a year after an uninsured crash, regardless of fault, to ensure future compliance.

4. SR-22 or financial responsibility filings: Before driving privileges can be restored, you may need to file proof of future coverage for multiple years, often three or more, at a substantial cost.

5. Higher insurance premiums: Once reinstated, insurance companies typically classify you as high-risk, increasing premiums by 100% or more for years.

6. Potential criminal charges: In cases where injuries or fatalities occur, driving uninsured can elevate the offense to a criminal misdemeanor or felony, with severe penalties including jail time.

Understanding these stakes highlights why even a minor accident without insurance can spiral into long-term financial and legal burdens.

How to Fight a No-Insurance Ticket?

It’s not impossible, but fighting a no-insurance ticket requires solid evidence and is only successful in limited scenarios:

- You had valid insurance, but the state’s electronic system hadn’t updated or had errors.

- The policy was active during the stop but canceled shortly afterward due to administrative or payment issues, with proof that the lapse wasn’t intentional.

- The vehicle wasn’t being driven at the time (parked, sold, or not operational), so insurance wasn’t required.

- Law enforcement made clerical errors, like incorrect vehicle identification numbers or registration info, which can invalidate the ticket.

- You took immediate steps to obtain insurance after discovering a lapse and can show good-faith efforts.

Buying insurance after receiving the ticket usually doesn’t help. Success often depends on official documentation from your insurer and DMV, and sometimes legal assistance, especially in states with strict rules and heavy penalties.

While these scenarios are typical in many U.S. states, no-insurance laws aren’t universal. Each country and province sets its own standards and penalties. To see how this issue is handled north of the border, the following video breaks down a no-insurance charge in Ontario and how drivers can fight it in court.

Don’t let an uninsured driving ticket derail your life or career. Whether you’re a daily commuter or a professional trucker, keeping your insurance current is the simplest way to avoid costly fines, license suspensions, and legal headaches.

Stay protected, stay legal, and keep your wheels moving.